There are facts and there are myths.

There are truths and there are lies.

There are bears and there are bulls.

There are some lies that select members of the financial and real estate industry would love for you to accept as fact. Real estate agents, brokers, lenders, appraisers, contractors, bankers and anyone else who profits from a transaction has a motive to spew lies to the public for their own personal gain. Whether or not they take action to spread those lies is what distinguishes those with ethics from those without.

What’s obvious to fiscally responsible, clear-headed people may not be as apparent to the millions and millions of sheeple who blindly accept the lies told by the National Association of Realtors. The NAR is certainly not the only party with incentives to lie, but they are by far the biggest in number since everyone and their brother seems to have a real estate license these days. I will proceed to pick apart 10 popular RE myths.

Myth # 1 – Real Estate Always Go Up!

While the price of a property may go up over time, its value does not. The price increase correlates with the increase in income and inflation over time. A $85,000 house in 1974 could be worth over $300,000 now, but people also have a higher income than they did 33 years ago. If you take into account maintenance costs and the wear and tear of the property, its value has actually decreased over time because it’s a much older house.

Myth # 2 – What About the Tax Advantage?

You wouldn’t buy an item simply because it’s on sale (well, some people do). Buying a house just for the tax advantage is like buying a Gucci handbag because it’s 30% off. It’s 30% off of what price though? The tax break for the mortgage interest paid is on taxable income. The borrower must have interest expenses greater than the standard tax deduction before he/she can benefit from the tax break. The tax break is nice, but barely offsets the extra costs of homeownership like insurance, maintenance and property taxes.

Myth # 3 – There Isn’t Any More Land

This statement in and of itself is actually true – we’ve explored all corners of the world. However, it’s misleading to use this as an argument to justify home purchases. People live in housing which lies on land. Housing can be a rented apartment, a townhome, a condo, a single family home or a mansion. Just because everyone wants to live in a McMansion doesn’t mean they should or could do that. Last I checked the United States has a lot more land than Hong Kong, Japan or most European cities. No one is going to become homeless due to the lack of land. That’s just absurd.

Myth # 4 – If You Don’t Buy Now, You’ll Be Priced Out Forever!

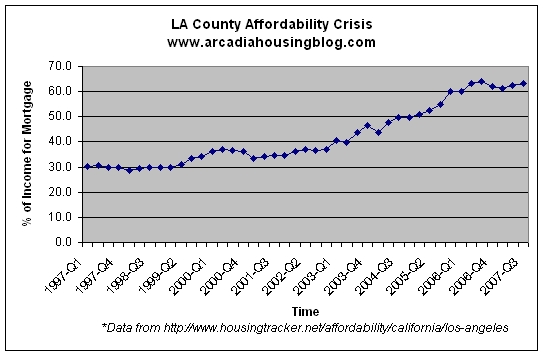

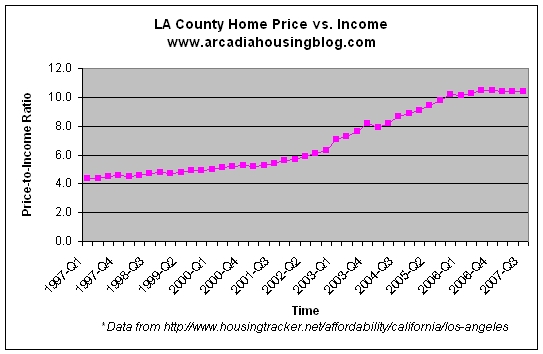

You have got to be kidding me. Isn’t this what they said during the last bubble, and the bubble before that and the bubble before that bubble? The double-digit growth outside of market fundamentals is simply unsustainable. Just like the previous two US housing bubbles, we’re in for years – not months – of price and volume decline. We’ve already seen volume drop off a cliff and guess what, price is right behind it.

Myth # 5 – You’re Wasting Money When You Rent

It makes sense to buy only when it costs about the same or less than it does to rent a similar place. During the past few years, it costs thousands more per month to “own” than to rent. The money saved from renting is better off invested in a higher yield market. Real estate agents tell you that by renting, you don’t get to build any equity. While that may be true, renters can make a risk-free return on their money with CDs and other savings accounts. Homeowners on the other hand wake up in the middle of the night worrying what the 15% price reduction on their neighbor’s house will do to their so called equity.

Myth # 6 – Real Estate Is a Great Investment

Contrary to popular belief, real estate is a poor investment. Real estate only averages 3%-4% annual return excluding inflation. Factoring in inflation, there’s almost no gain (+0.7% per Shiller study) in home ownership over the long run other than the shelter and warm and fuzzy feelings it provides. Things change when there’s a bubble, but bubbles are by definition unstable. CDs are running at 3.65%, the stock market at 8% over the long haul and 10%+ for slightly riskier index funds. On top of that, cash, stocks and funds are highly liquid. Real estate is the exact opposite – if you can’t find a buyer, you are stuck holding the bag.

Myth # 7 – Everyone Wants To Live In California

Ah yes, the omnipresent sunshine tax of California. Sure the weather is nice, but standard of living is horrendously high. Compared to other states, you don’t get much for your money when it comes to housing. Maybe that’s why our great golden state has experienced a net outflow of people over the recent years. There are more young and middle aged families moving out of California than moving in – citing affordability as the main reason. Besides, if California is so special, then prices should never drop right? It dropped for 7 consecutive years in the early 90s before prices hit bottom.

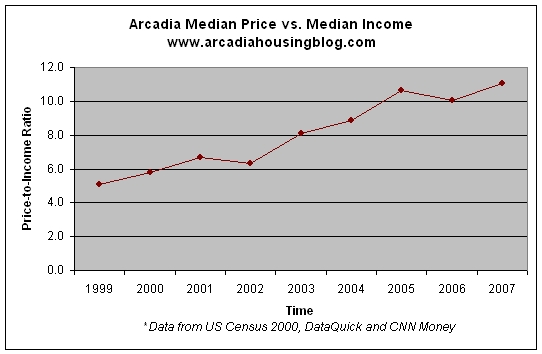

Myth # 8 – Many Rich Asians Can/Will Buy with Cash in Arcadia

Although Arcadia has a high population of Asians, that doesn’t mean they’re all wealthy. Even if they are, they surely didn’t get wealthy by being dumb. As crazy as this sounds, they know something about money too! Why would they buy when they can rent for much cheaper? Even if they have enough dough to buy in cash, why wouldn’t they just put down enough to get a good interest rate and borrow the balance while investing the difference in a higher yield, low risk market? Just load up Redfin and take a look at the map. There are many, many homes for sale in 91006/91007. Asians are notorious for their bargaining skills and I’d imagine they’ll use those skills when purchasing a home.

Myth # 9 – Rent Will Increase Over Time

Yes, but again, rent is directly correlated to income and demand. Rents can’t skyrocket just because the landlord feels like making an extra buck if there’s no market for it. The renters can only afford to pay so much based on their disposable income. If income in the area does not increase dramatically, rent cannot and will not move much. Moreover, if demand is a reason then it actually builds the case not to buy because if so many people are buying homes, then demand for rentals is small because so many people are home owners.

Myth # 10 – Many People are on the Sidelines Waiting to Buy

With the record high rate of home ownership posted by the Bush administration, it’s clear many people bought during the boom. These people are no longer potential buyers so the buyer pool has shrunk. All the debtors who have or will default are also out of the buyer pool for the next 7 years due to bad credit. There are only so many people left on the sidelines. On top of that, these sideline buyers will have to go through much stricter lending standards since the credit market is much more risk adversed now – as they should be. That means they’ll need to have 20% downpayment, good credit, assets, relatively low DTI ratios and documented income. There aren’t too many people with those qualifications on the sidelines.

I’m not saying never buy a house. There are good reasons to buy a house, but none of the above qualify as a good reason. Instead, they’re all lies told by the industry insiders to boost their earnings.

So…

There are facts and there are myths.

There are bears and there are bulls.

Can you see why they call it bullsh*t?